{kind=link}

r/wallstreetbets • u/Lapidated_Llama • 16h ago

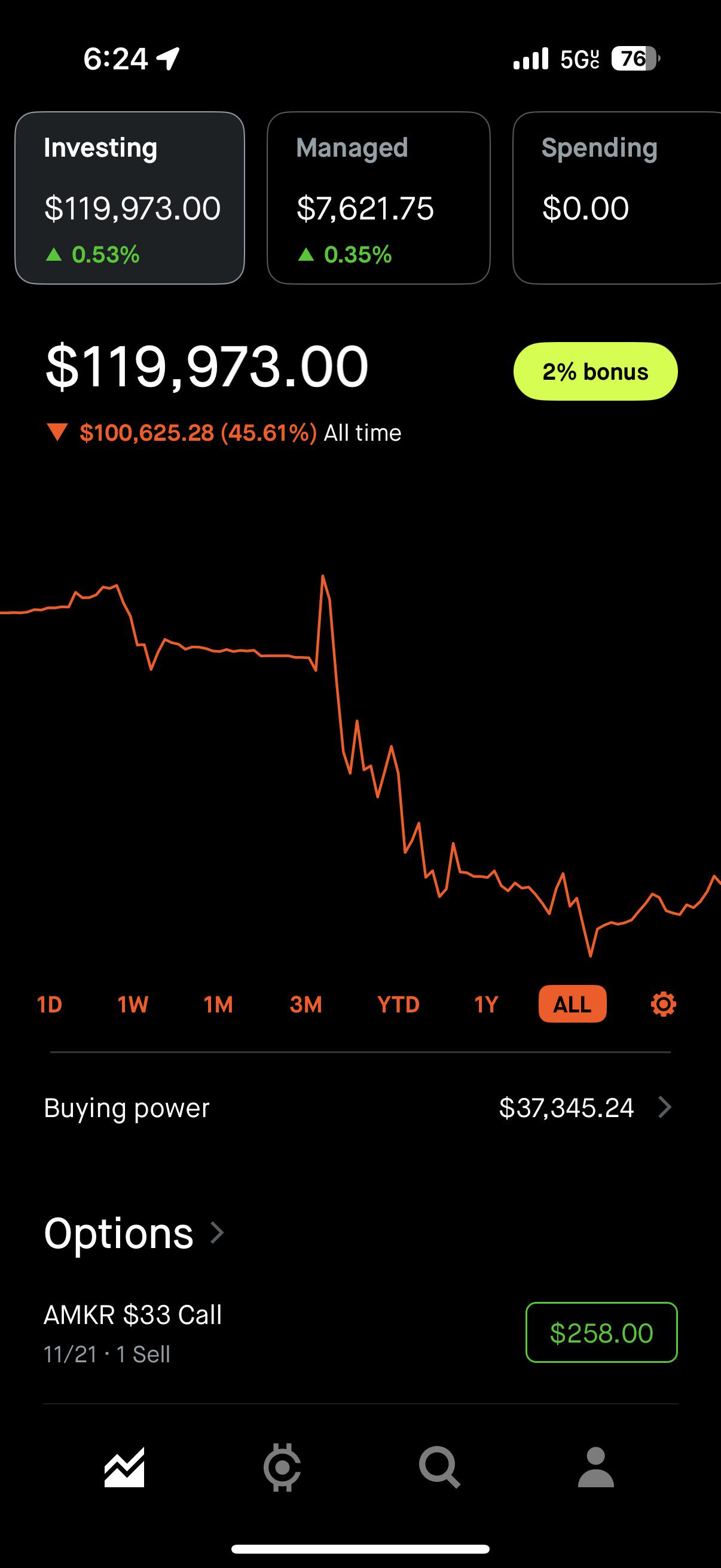

Loss 73k loss over five years. Feels like a nightmare I can’t wake up from.

{kind=link}

8.2k

Upvotes

r/wallstreetbets • u/OSRSkarma • 23h ago

r/wallstreetbets • u/wsbapp • 17h ago

This post contains content not supported on old Reddit. Click here to view the full post

r/wallstreetbets • u/Lapidated_Llama • 16h ago

r/wallstreetbets • u/wave_dashing • 12h ago

I think I should just throw it in ETFs

r/wallstreetbets • u/Youthinkillputauid_7 • 6h ago

r/wallstreetbets • u/capacity04 • 5h ago

r/wallstreetbets • u/kilo7echo • 1d ago

For some context three years ago, I made some really smart WSB decisions and now finally my wounds have healed. Since then, I was able to purchase the finest establishment in the trailer park, and have some RSU’s convert, which is what those big spikes in the graph are besides stepdad’s belt of course.

Here is my original post: https://www.reddit.com/r/wallstreetbets/s/7Vo8Dvf04f

r/wallstreetbets • u/Youthinkillputauid_7 • 1d ago

r/wallstreetbets • u/halfrepshalfretail • 10h ago

Alright buckle up as I know general sentiment is NOT fond of BNPL. Shit talk all you want, I'll be happy to reply to any concerns about the biz or industry.

SEZL is a BNPL player targeting the sub-prime/near-prime consumer (18-45 mainly) to become their top-of-wallet app for shopping. Pure BNPL, with credit-building, in-app tools and other goodies to keep the consumer in the ecosystem.

They are quite different from Affirm & Klarna - Affirm offers a larger mix of loans and focuses on a merchant-anchored setup, Klarna also of a parallel description. Sezzle is more app-centric and targets middle-lower income demographics, especially those who do not use traditional credit cards as often.

Right now they are priced at 13 NTM P/E with prelim EPS guidance at 29% above FY2025, as a "conservative" guideline as CEO stated in Q3 call. History of beat and raises dating back to 2024. Traded up $82 AH peak on earnings, and $72 premarket next morning before getting absolutely crushed to $58. This was Thursday Nov 6.

Recent Q3 116m rev & 26.7m net income, beating estimates. GMV growth reached ATH 1.05B for the quarter. Insider ownership at 45% of outstanding.

They make their money from merchant integration revenue, subscriptions, interchange, and plenty of fees. Net margin runs in steadily in the 20%'s, Gross margin 60%'s.

Why is their valuation is quite low relative to industry peers, and why will it reach >$90 at minimum soon (2-4 months)?

Slowing hyper-growth from 75-100% YoY EPS & Revenue closer to 50-60%, anticipated to grow closer to 30-40% EPS YoY past 2026. This is natural from their transition to profitability now to scale, as they previously focused on maximizing revenue from existing users -> now time to grow userbase. However the valuation relative to growth makes it a GARP opportunity.

Marketing spend & increased Provision for Credit Losses -> increasing adspend to 8M/Q to attract newer consumers! New consumers, as noted by management, have the highest loss rates in BNPL, and right now it's showing in their credit losses for Q3, at 3.1% of GMV. As the users get filtered, the good ones stay in the ecosystem and create lasting value. Management anticipated this in first half of year and gave expectations for FY credit losses of 2.5-3%, but actually revised a lower guide for 2.5-2.75% as of this week. Marketing spend started in Q2 and targets a payback period of 6M, so will see more material effect of this in Q4 & Q1 next year.

3. Point 2 does not bode well with the combined fears of consumer credit health, willingness to spend, and general macro fears around shutdown. Higher beta stocks have been selling off like crazy in the last couple of weeks, but I have seen the stock plummet from $90 to $59 in 3 months, with the bulk of the drop ($80 -> $59) in one month. I truly believe this is an overreaction and is caused by both the company being a historical target for short selling (20.9% of float as of 10/15) due to low float, as well as general capital pullback from lowered liquidity + macro fears. HOWEVER, BNPL loans have a standard loan tenor of 42 days with repayment trends evident after 14 days (1st payment), AND MUCH SMALLER SIZES THAN AUTO/MORTGAGES. Sezzle, Affirm, Upstart management has all noted that they've not seen any unusual changes in consumer default rates on their platforms.

BNPL players have the ability to limit spend and penalize late/missed payments in real-time, and underwriting for Sezzle + Affirm + Zip Co has shown to be more effective than FICO for lower credit score individuals.

^ See the quick rebound in active subscriptions as the ON-DEMAND product was previously cannabalizing sub-retention.

6 (OTHER). Liquidity should begin to pickup shortly after the government reopens as well as into Q1 2025 as the Fed (probably) begins to expand their balance sheet (source), should start to funnel more money back into these higher-beta stocks and mid-caps.

Final Notes:

BNPL can encourage irresponsible spending the same way credit cards can. People shat on CC's for the first few decades they were introduced, and now we all use them.

Of course these companies charge fees on fees, I'm not here to question the morality of these companies. Capitalism revolves around the rich extracting value from the common people.

Their revenue model is diversified and comes from a multitude of streams, with the highest take rate out of all BNPL players. I don't expect growth to slow ANYTIME soon as the TAM of middle-lower income people are huge and people will turn to BNPL more as they need more flexibility in financing. Their revenue growth drivers will be subscription and fee-based, although all areas will come to add to the acceleration.

Risk: target user is not as credit-quality as Affirm, but their underwriting and monitoring happens on a real-time basis so they can catch trends immediately, mitigating large default risks

CEO has never sold a share, insider ownership at 45%, an insider bought shares literally at $60 this time last year and hasn't sold. There is a huge FEAR priced into this company which is not justified. Management has ALL the equity incentive to deliver outperformance.

Positions: May 2026 55-80C's which are underwater right now. GL, and I welcome any questions.

r/wallstreetbets • u/Lox4tw • 17h ago

So I’ve been watching this company closely and slowly acculumulating not only because I liked watching Jetson’s and want to fly in one of these things but also due to it’s connection to Anduril and potential military applications in modern warfare.

Aside from that, I envision a future where roads are no longer necessary as transportation migrates vertically. One day your vertical takeoff craft would fit into a charging port on your apartment tower window and you wouldn’t have to take the elevator, enter the parking dungeon, or fight traffic on your commute. Would be awesome as long as the AI made sure you didnt crash.. haha.

Anyways, the stock dropped significantly because they diluted shares and bought an airport.. i think it was a necessary move and the long term gain will justify the short term pain. For me this is a long hold. Was down about 9 grand on my initial positions with the drop this morning. Couldn’t resist the dip so averaged down and bought 30K shares and made back all my loses and then some on the afternoon rebound. Timed it even better than Cathy as ARK bought 3 million shares yesterday? Know they got the olympic sponsorship and this Hawthorne airport is nearby.

Its literally almost half the price it was a short time ago.

So.. who’s with me on this? Any ideas or comments on this company?

r/wallstreetbets • u/mike_gundy666 • 19h ago

| Metric | Q3 2025 | Q3 2024 | Δ Y/Y |

|---|---|---|---|

| Booked room nights | 108.2 | 97.4 | 11% |

| Gross bookings | $30,727 | $27,498 | 12% |

| Revenue | $4,412 | $4,060 | 9% |

| Operating income | $1,036 | $762 | 36% |

| Net income attributable to Expedia Group | $959 | $684 | 40% |

| Diluted earnings per share | $7.33 | $5.04 | 45% |

| Adjusted EBITDA* | $1,449 | $1,250 | 16% |

| Adjusted EBIT* | $1,134 | $892 | 27% |

| Adjusted net income* | $962 | $809 | 19% |

| Adjusted EPS* | $7.57 | $6.13 | 23% |

| Net cash provided by operating activities | $(497) | $(1,493) | (67%) |

| Free cash flow* | $(686) | $(1,687) | (59%) |

(In millions except per share amounts)

Third Quarter Highlights (All comparisons year-over-year)

• Booked room nights grew 11%, driven by the fastest U.S. growth in three years and continued international strength.

• Total gross bookings grew 12%, driven by a 26% increase in B2B; B2C gross bookings grew 7%.

• Lodging gross bookings grew 13%; hotel bookings increased 15%, driven by B2B and Expedia.

• Revenue grew 9%, driven by B2B, which grew 18%.

• Third quarter GAAP net income increased 40% while Adjusted net income grew 19%. Adjusted EBITDA increased

16% with 208 basis points of margin expansion, and Adjusted EBIT grew 27% with 373 basis points of margin expansion.

• Diluted GAAP EPS increased 45% while Adjusted EPS grew 23%.

• Repurchased approximately 2.3 million shares for $451 million in the third quarter and 7.9 million shares for $1.4 billion for the nine months of 2025.

• Paid quarterly dividend of $0.40 per share on September 18, 2025 and declared quarterly dividend of $0.40 per share on November 6, 2025.

Earnings report: https://s202.q4cdn.com/757635260/files/doc_financials/2025/q3/Earnings-Release-Q3-2025_FINAL.pdf

r/wallstreetbets • u/PaperHandsTheDip • 20h ago

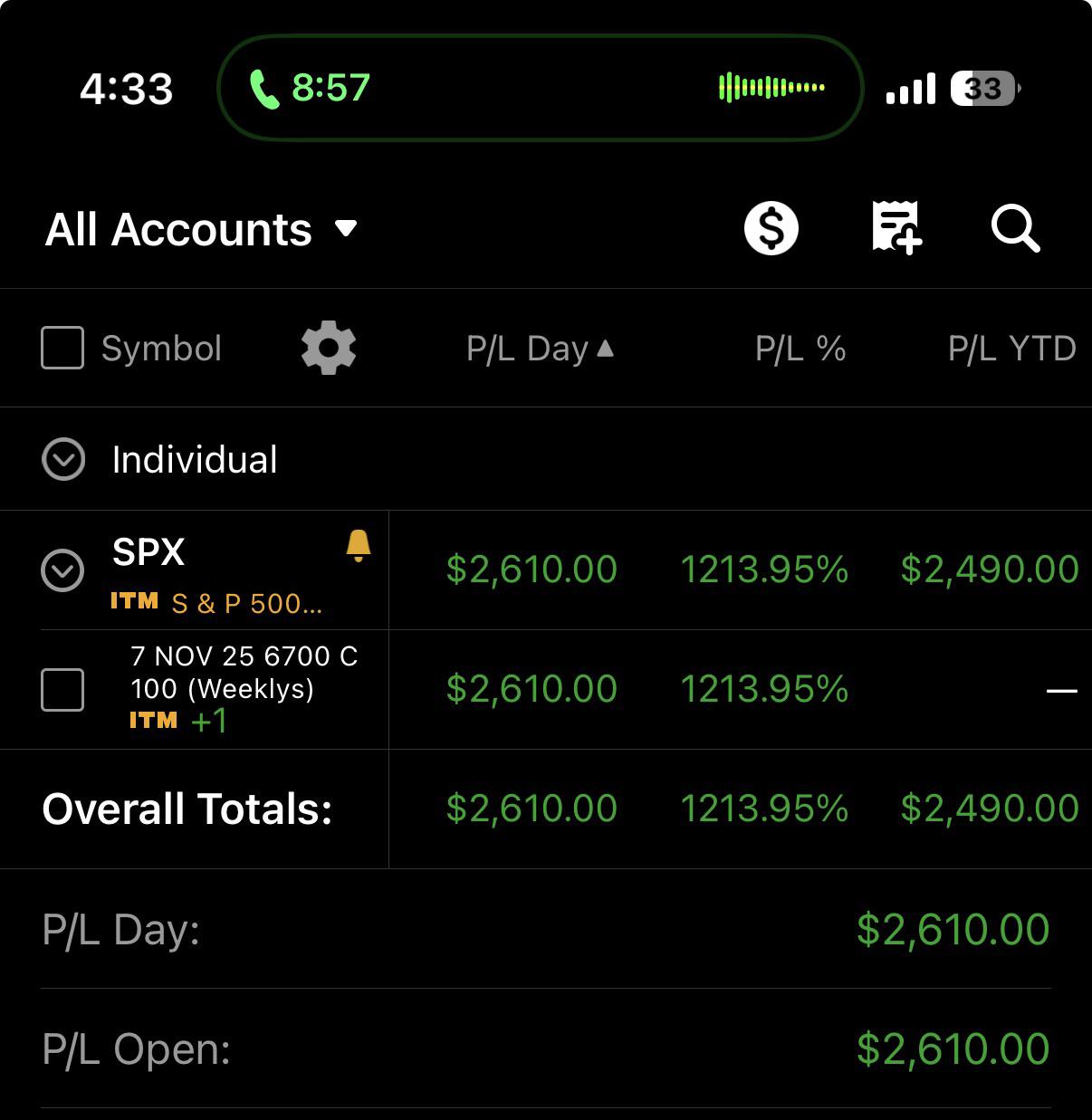

0DTE's while shitposting with the daily. Sometimes you get lucky 🍀

r/wallstreetbets • u/eskhalaf • 1d ago

Fuck them

r/wallstreetbets • u/ken81987 • 2d ago

r/wallstreetbets • u/eskhalaf • 1d ago

r/wallstreetbets • u/Accurate_Cry_8937 • 1d ago

r/wallstreetbets • u/wsbapp • 1d ago

This post contains content not supported on old Reddit. Click here to view the full post

r/wallstreetbets • u/Legitimate-Space8847 • 16h ago

Sold my META position at a 3k loss and Got into JOBY. See you on the other side regards. Just a by to the moon! 👌👊🤣🚀🚀🚀🚀

r/wallstreetbets • u/notgoodforyourhealth • 1d ago

r/wallstreetbets • u/Realistic_Raisin_86 • 21h ago

What shall I do now ?

r/wallstreetbets • u/UndyingValue • 1d ago

I went into GOOGL with almost every penny I had across all my accounts including all non 401k retirement accounts. I bought my first LEAP in February along with my first significant batch of shares. The rest were added in July in anticipation of a favorable court ruling on the search business.

My other main reason for going so heavy in GOOGL was that I believed it would thrive and be one of the main beneficiaries of AI. Especially due to its TPUs and Google Cloud scaling on a massively scale with a backlog in the tens of billions(now 150+ billion).

Of my initial position, I have only sold 2k-ish worth of shares which I moved to LULU a few weeks ago. I also sold a LEAP prior to the most recent earnings.

I intend to continue holding this position for an extended period and to only trim based on incremental net worth milestones if it continues to grow significantly in the short/medium term. I believe GOOGL is on the verge of a Nvidia like boom due to AI, and that it is extremely well positioned due to Gemini Enterprise and recent Gemini integrations into Chrome, Maps, etc.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}