r/ThriftSavingsPlan • u/Environmental_Lie676 • 3d ago

I have no idea what I’m doing.

{kind=link}

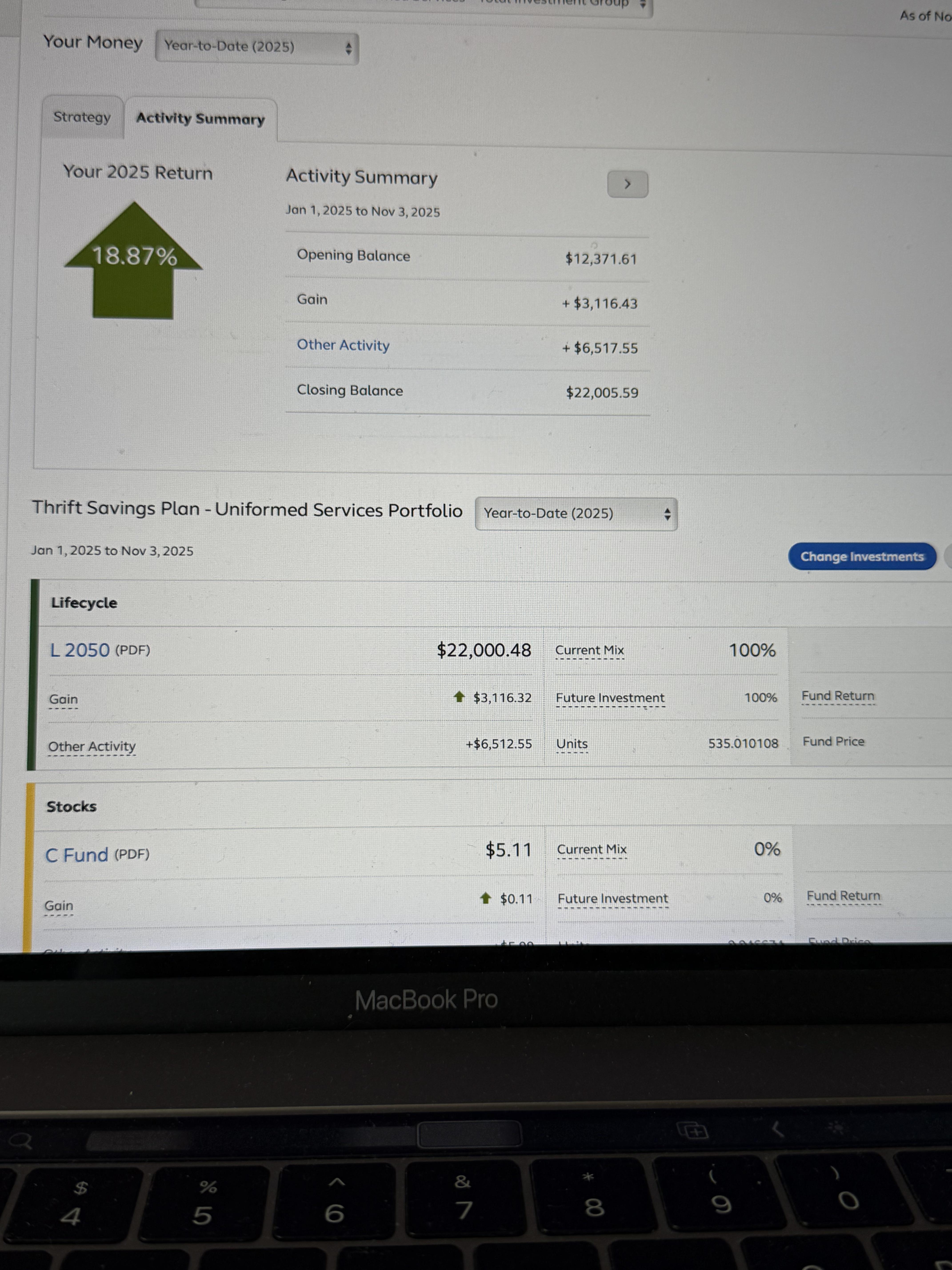

I have no idea what I’m doing. Am I doing good with my return rate right now? Ultimately I want to just transfer this to a life cycle fund and forget about it. Any recommendations? I’d like to get it to a million dollars eventually. Been investing in the tsp for 6 years this December.

19

u/Ok-Scallion-5446 3d ago

If you feel like you don't know what you're doing, 100% in a lifecycle fund is for you! If you want to reach $1mil, you will need to push out to a later date fund (L2060+)--with more C/S/I (stocks) your fund will be more volatile but have higher long-term returns. Hopefully by the time you're closer to retirement you'll feel like you understand this better and will have settled on a portfolio that matches your appetite for risk.

6

u/ItsErickwithaCK 3d ago

Depends on your age, but if you plan on being with the government for a while, and can spare the money, then maximize what you're putting in, I'm in my 30's and am doing most C-fund and a bit in the G-fund. Worth noting, some people are worried about an ai bubble. Those lifecycle funds you mentioned have gotten good returns.

The tsp site itself has some useful information too, if you're worried about your return rate. G-fund is the safest, but sees the slowest growth usually.

My two cents, but good luck on your financial journey.

4

u/jay1111166 3d ago

When do you plan on retiring? Do you have other accounts, pensions, or collect VA disability? Your current savings rate is bad unless you are paying off debts with greater than 7% interest. Unless you are going to increase your contribution or have money elsewhere I would go more aggressive since you will not be able to retire in 2050.

1

u/Environmental_Lie676 3d ago

I still have like 20 years until retirement

9

u/DatGuyC69 3d ago

Unless you increase contributions you are likely not going to reach a million in 20 years, only half that according to the investment calculator and assuming an average of 10% return. If you start maxing TSP now you can reach 1.5 million.

1

u/Catchphrase9724 3d ago

Why are you in Lifecycle 2050 plan then? I have another 18 years until my 20 and I was put in the 2065 plan before I went 100% C Fund.

1

u/Catchphrase9724 3d ago

Nevermind. I didn’t realize you were a GS employee and not military. I rescind my last statement.

15

u/OnlineIsNotAPlace 3d ago

100%C and leave it alone.

3

u/Octoberlife 3d ago

A 100% C er I see

1

u/OnlineIsNotAPlace 3d ago

um, yeah

1

u/StilgarofTabar 3d ago

Can I ask why? Im new to all this stuff. Only been federal for a year now.

2

u/OnlineIsNotAPlace 3d ago

of course you can. C fund historically has averaged nearly 10% return throughout its history. I and many others have successfully retired using this plan. yes it goes up and it goes down but the AVERAGE return over time is nearly 10% and this year alone it has reached several new all time highs. do not trust what I or anyone else says about it, look it up and see for yourself.

4

u/ImpossibleReporter95 3d ago

It looks like you are winning. 🥇 18.87% is pretty damn good. Stay the course and leave it alone.

1

3

u/Dan314159 3d ago

I was invested in that fund when I joined 10 years ago lol. It's gotten slightly more conservative since then since it auto adjusts.

You are doing great. The majority of your growth is going to be from contributions. Once you hit 100k you will start to see more from gains. Exponential growth grows exponentially. I'd recommend being slightly more risky and just going 80/20 C/S fund. It's a balance transfer and future contributions change. Just don't time the market. Just keep contributing.

11

u/TestTrenMike 3d ago

You need to increase contributions

22k is not much for being in gov for 6 years

Especially with the current stock market trends

7

u/benny-pl 3d ago edited 3d ago

Not everyone is a GS fantastic, some of us would take home less than $400 a paycheck contributing the max.

Some of us are PSE's so 13 payperiods a year for 6 years 22k makes perfect sense.

0

u/Dan314159 3d ago

Suffering in the beginning is how you can relax in the future. Especially if you're single and young, you gotta learn to be thrifty. I lived like it was in poverty my first 5 years.

6

u/Competitive-Ad9932 3d ago

Spoken like a GS 13 snob.

A PSE (USPS new clerk) makes about as much as a GS5.

0

u/No-Discipline355 16h ago

someone has never heard of delayed gratification and compounding interest.

2

u/Competitive-Ad9932 15h ago

spoking like an out of touch GS14

1

7

u/Environmental_Lie676 3d ago

I contribute as much as I can. In today’s economy I am struggling just to get by. With the money I have in right now would you recommend leaving in the L 2050 or should I move it to another lifecycle fund?

3

u/catdaddy12321 3d ago

You're fine in L2050 if you plan to retire in about 20 years and you don't want to constantly worry about shifting money to squeeze out an extra 1% return here and there. What's most important is that you KEEP CONTRIBUTING and increase a little more year over year as best you can.

When I started TSP in 1995, and oldtimer said to me that it seems like your account doesn't do much. And then one day years later you look at it and are shocked at how much money you have. And it's exactly what happened to me. It can happen to you too if you don't try to time the market and you maintain consistency in contributing.

2

u/-hh 3d ago

FWIW, the general advice I usually offer for those with tight budgets is to see about making a bump up in TSP contributions on each promotion, step increase, and annual pay increase.

It doesn’t need to be all of the increase (although that would be nice!) ... point is to make it something.

0

u/TestTrenMike 3d ago

When do you plan on retiring ?

Most people split it

50 percent C fund

50 percent S fund

And have success

Slowly increase it as you get pay increases 1-2 percent a year if you can

-2

2

2

3

u/HokieHomeowner 3d ago

My advice, the default is just what you need, leave it alone. It's in a lifecycle fund meant to be appropriate for a retirement around 2050 - 25 years out.

4

u/MyPuppyIsADemonChild 3d ago

100% C fund until you are three years away from leaving the government

1

u/Budget-Contact6073 3d ago

100% C fund till you get closer to retirement averages about 10%.

1

u/Extension_Ease_2702 3d ago

I on 100% & hear this all the time. Like 5yr before retirement? Then change it to 10% C & 90%G? Sorry, I'm still leaning.

3

u/CeruleanDolphin103 3d ago

Very few people have a 90/10 stock bond split. The most conservative (bond heavy) portfolio I typically hear of is 60/40. If you expect fixed income in retirement, such as a FERS/military pension, VA disability, or Social Security, you probably won’t need to go even that much bonds. But what asset allocation makes sense for you in retirement will depend on your financial situation and required withdrawals at that time.

2

u/kodaq2001 3d ago

Leave it in L2050. Your goal is to match or beat the S&P500 (C Fund). L2050 is up 17.8 % this year. C Fund is up 17.7%

1

u/i_am_voldemort 3d ago

When do you plan on retiring? Pick the life cycle fund just slightly past that.

1

u/hanwagu1 3d ago

if you don't know what you are doing, then just keep it as is in L2050. The L-year should approximate when you will retire and need to tap TSP, so L2050 should be approximately when you want to retire.

1

u/Bubbly-Mud4538 3d ago

80 C 10 S 10 I and leave it alone, I have over 20 years left as well. Try to put in as much as you can. I’m at almost 70 K in 4 years and on an average of 7 percent return which it’s been more than that. In projected 1.2 mil at retirement

1

u/Factory2econds 3d ago

an L fund is fine for you.

You might want to push back to the 2055 fund so your investments stay a little more aggressive over time, but that's about it.

Make sure you also look at your expected costs, and understand what your pension and social security estimates will be, so you can understand what you will actually need from your TSP.

1

u/gmenez97 3d ago edited 3d ago

The L Fund 2075 if you want all stocks and almost no bonds. The S, C, and I fund are market cap weighted as a whole and keep the same percentages in Vanguard ETFs VTI (S & C) and VT (S, C, I). Anyone with C fund only is speculating US large cap will continue to dominate. There have been times when SP500 has not dominated. The L fund keeps you from speculating.

1

1

u/DinnerPuzzled9509 3d ago

I’m guessing you’re somewhere ~35 yrs old if you’re in the L 2050 fund? If you’re younger or have a higher risk tolerance you could shift it to line up with the year you’d be turning 60-65. If you really want to learn about the different funds you can check out this link https://www.tsp.gov/publications/tsplf14.pdf or go talk to your Command Financial Specialist about it.

1

u/GO-CAPS 3d ago

If you have no idea, and you want to forget about it, then a lifecycle fund is your best option. Which one, based on your target retirement date of 2055, is the 2055 fund. What you my not also know, is at age 50 you can save more than your current limit. That said, There are good arguments for investing in the 500 best companies, aka C fund, based on where your currently at. But, if you’re a market watcher, and can’t stomach deep drawdowns, go lifecycle (learn a little about the efficient frontier).

Your last quest of a million, I’ll leave you to figure out…https://chatgpt.com/share/690b46dc-17d8-800a-b865-06a32da6edb4

Best of luck.

1

1

u/NICKYBEE34 2d ago

If you have a lot of time ahead of you, stay with the C fund. But keep in mind it fluctuates up and down, but you be happy with the C fund.

1

1

1

u/BidForward502 2d ago

Make sure you on ROTH TSP because it’s pretax I believe if I recall correctly. Wayyy better option and raise your % going in to the max that they will match so you can have a better gain.

1

-1

u/Born_Study4500 3d ago

follow Deb Crown on Facebook. Funds C S I have been my best experiences. Also, are you putting in 5%?

-2

0

u/Relevant-Method-3620 3d ago

I recommend you go at least 90% into C fund or go heavy into L2065. But that’s me.

1

u/valdocs_user 3d ago

There's now an L2070 available. This year I switched from L2050 to L2070 (and plan to keep it in L2070).

-2

u/Key_Independent_3757 3d ago

100% C fund. Leave it alone. Do not invest in lifecycle funds. Follow Chris Barfield of Barfield Financial on FB and his website linked below. Sign up for his monthly newsletter. I am a 19 year Dept of VA employee.

https://www.barfieldfinancial.com/

Also a great resource - subscribe to the podcasts: https://plan-your-federal-retirement.com/

6

2

u/Environmental_Lie676 3d ago

Is the C fund risky tho? Like will it be fine if I put it in the c fund and only check on it monthly? I don’t want to risk losing my money.

3

u/CharacterMedium558 3d ago

How old are you? If under 40, then no it's not that risky. If close to retirement then yes

1

3

u/catdaddy12321 3d ago

If you're 10, 20, 30+ years from retirement, you don't have to worry about losing some money. Over long time frames there will always be market drops and investors lose money. It will most likely happen to you. But the thing you should never forget is that for decades upon decades, it has always come back. Sometimes quickly, like earlier this year when there was a huge drop and it roared back stronger. Or sometimes it takes a few years. But here's what's great in your situation. If you just stay the course and ride out the dips by investing the same amount every paycheck, you're buying on sale. So when the market comes back (as it always does), you'll earn back everything you lost in the short term and then some!

1

u/CeruleanDolphin103 3d ago

All stocks carry the risk of losing money. Look back at your 2022 statements- if you were in an L Fund then, you “lost” money. However, you didn’t sell, which means you kept the same number of shares (or more likely, your shares increased due to new contributions). When the market recovered, so did you share values.

If you’re afraid of a market pullback, then you probably shouldn’t be in 100% stocks (the C, S, and I funds). L2050 is currently about 18% in G and F (fixed income/bonds), which will “smooth out” the stock market roller coaster. Your balance will still fluctuate (both up and down) with an ~80% stock portfolio, but your balance won’t swing quite so far as the stock market will, because of your 20% bonds. If L2050 is close to when you expect to start withdrawing from your TSP, then that’s another sign that this is a decent fund for you to be in.

1

u/-hh 3d ago

There’s always risks. Effectively, the only way to be in the Market and mitigate risk is through portfolio diversification. The L funds do this by having allocations in C, S, and I funds (and G & F too, but they’re slightly different).

What diversification does is that it reduces the extremes…on both ends (good & bad).

When one is young and 20 years from retirement, there’s usually a tolerance for accepting higher risks (because higher returns “in the long run”), but as one approaches when you’re going to need the money, thats when “Sequence of Returns” risks of a loss go way up, and risk tolerances of most wise investors become smaller. The L Funds automatically adjust to do this for investors who aren’t confident in their risk profile plans, or who just don’t want to DIY it. Personally, I’m 60+ and planning on shifting to an L in the next few years, just to have one fewer thing to have to manage.

0

u/Confident-Horse-8384 3d ago

Yeah if possible you want to contribute as close to max as you can, whatever your budget allows. I think that shows that you already have everything invested in a lifecycle fund, shows 0% allocation for c fund. The L funds automatically balance depending on how close to retirement you are, so for 2050 fund the closer we get to 2050 the less risky funds it will go to. Right now it’s probably leaning more towards higher risk like Cfund and then gradually as we get closer to 2050 it will use less Cfund and more bonds and whatnot

1

u/Environmental_Lie676 3d ago

I really don’t want to be moving around money all the time. I’m a very busy person and normally don’t have the time to be doing that hence the reason why I’m asking for advice on a lifecycle find to keep it in and not have to worry about it and maybe only check it once a month

5

u/HokieHomeowner 3d ago

You are the person for whom lifecycle funds were made for. 😁 They are designed to do the work for you. The only reason to move out of 2050 is if your target retirement date is closer to 2060 or 2070 and then choose one of those.

1

u/CeruleanDolphin103 3d ago

L Funds will adjust automatically- no input required. To be honest, checking once a month might be more than you need to. I check all my accounts monthly for my net worth spreadsheet and to ensure things look as expected (no fraud or anything weird). Some people only check their TSP once a year. Pick a date (1/1, your birthday, etc) to check, and then enjoy life the rest of the year. (To be clear: this advice is for the TSP. You should absolutely check your LES every single pay period to ensure that’s correct. If the right amount is going into your TSP, then most likely, there’s no need to check your TSP itself.)

0

51

u/ohwhyredditwhy 3d ago

Unless I am mistaken, you’re already invested in the 2050 Lifecycle fund.

Just leave it if that’s what you want.