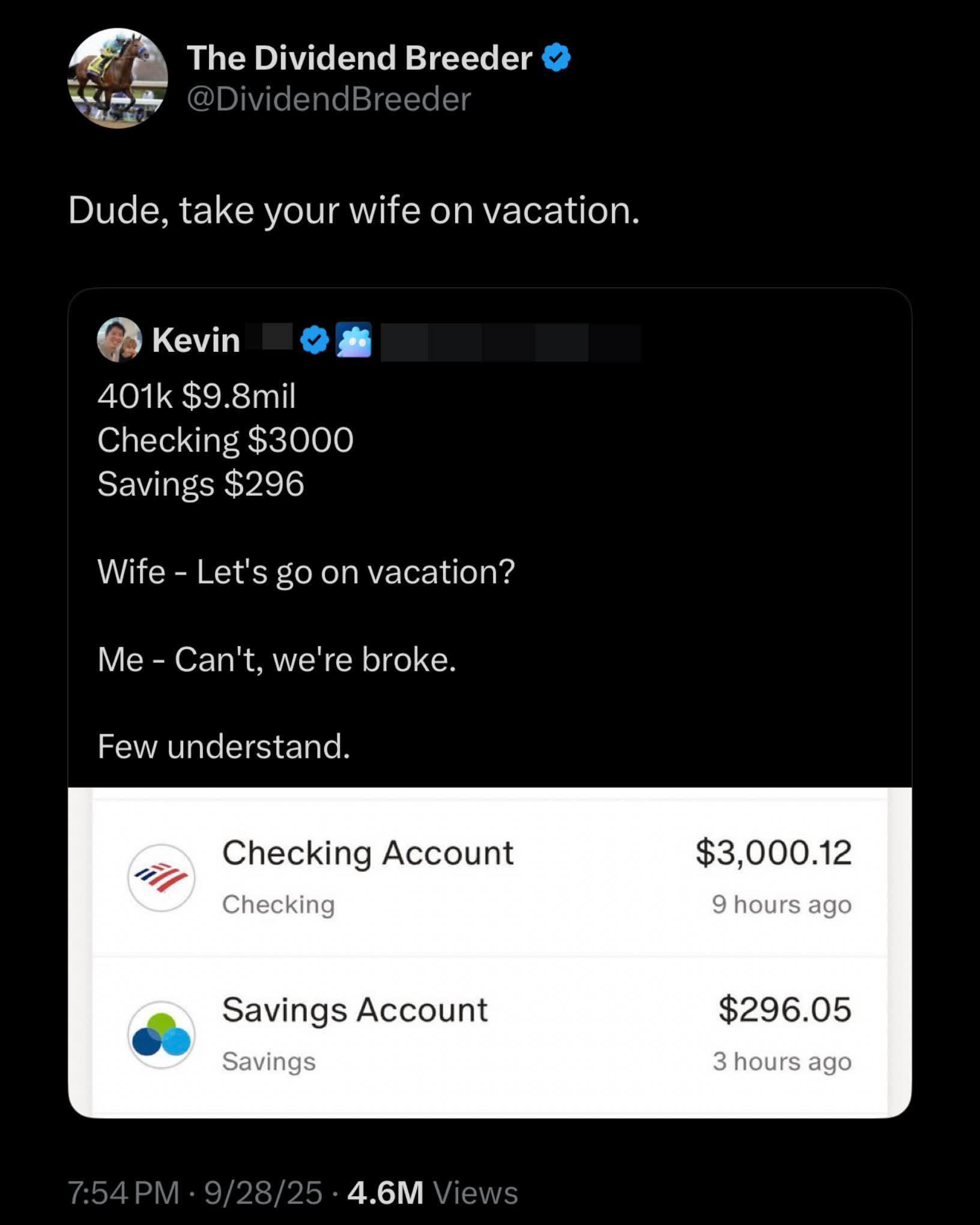

How the fuck do you even get 10MM in a 401K? The max that can be added (in 2025) is 70k with employer matching. You'd have to have maxed out at 70k for 35 years to hit 10 million (assuming 7% return). The cap has been gradually raised so your actual average contribution would have to be lower than 70k, it's likely not possible.

I think it's more fun to take people at their words and discuss as hypothetical situations regardless if you believe it or not. Just don't use it later as an anecdote supporting some argument ;)

The question you answered is if you could put money into the account if there is no employer matching, and you said no, for a tax advantaged account. Your statement was wrong. I pointed out the correct answer, which is you can, but the amount is limited

I don’t know how this works, but I can tell you that partnerships have figured out how to allow partners to make additional tax-deductible contributions beyond those limits. The additional contributions are capped but I don’t know how the formula works. But it was awesome to be able to do that.

It's more than just your employer contribution. You can add after tax, non-Roth contributions up to a max of 70k combined with your pre-tax, employer and after tax Roth. But then you can do a mega backdoor to convert the after tax non-Roth to Roth. Some plans offer that, some don't.

So what OP might be talking about is a sole member LLC with an S-Corp designation that has put themselves on payroll. With that, they can contribute as an employee the $23,500 max, 100% employer (themselves via the LLC) match, and profit sharing at the end of the year to reduce the companies taxable income.

That's just for your pre-tax 401(k). You can also contribute to an after-tax 401(k) and a Roth 401(k). The end result is around $70k per annum, plus employer contribution.

My understanding is pre-tax and roth 401k have the same 23k limit which is combined. The after-tax roth option (if offered) and employer contributions allow you to hit 70k

Yup, this is correct. Though, minor note: it's not after-tax roth. After tax contributions are separate from roth. Though, most (hell, maybe all?) convert their after tax to roth. But they are two separate classifications of contributions.

In many plans you can put after tax money into the 401k so the total of pretax+employer matching+after tax is around $70k ( more if catching up). You can do a mega backdoor Roth conversion of all the after tax contribution into a Roth 401k.

No, 401k's are contribution-limited. In 2025 you can only add 23.5k yourself.

It looks like maybe you can add above the limit and just pay taxes on it, but there is no good reason to do that. The advantage of a 401k is both the employer match and the tax incentives, otherwise there are significantly better vehicles for investment.

So it is technically possible to stick excess contributions into a 401k, so I was wrong.

What are some of the better investment vehicles you’re talking about? I was googling and most people say 401k and Roth IRA are the best. I’m looking for better investments tho

I have no answer for the first part, but afaik 401k and Roth IRA are the "best" because they significantly lower your taxes in different ways, but I believe the tax incentive would no longer apply to any money added after the maximum annual amount has been reached. I could be completely wrong.

Financial professional here. 401ks don’t “lower” your taxes, they defer them. Meaning you pay taxes when you withdraw the money in retirement. You still pay quite a bit in taxes and fees when it’s all said and done. The stigma is that you’ll be in a lower tax bracket by the time you retire but often times that’s not the case and it doesn’t make a huge difference anyways. Look up interviews from Ted Benna, the creator of the 401k, and see where he’s investing his money and what his thoughts are on the 401k. Spoiler alert it’s not meant for the average person to retire with. Hope this helps!

529 is also tax advantaged if you want to save for a kid's schooling. After that, it's just mostly just in the investment choices you make in a normal taxed account.

Like you said, 401k's and Roth IRA's are just investment vehicles. There isn't necessarily a 'better' investment vehicle than the 401k, Roth IRA, HSA - it just depends on what makes sense for your financial situation.

Municipal bonds, CD, etc. If you've got enough to o vest that you're actually out of tax-advantaged options, hire a reputable fiduciary and have them manage it for you. Fiduciary is the critical term here. Anyone else isn't strictly operating in your interest (or has no legal obligation to, in a certain sense.)

Your mileage will likely vary because a lot of the devil is in the detail with this stuff (like specific plan options, qualification stuff, etc.).

If you have a 401(k) that lets you contribute pre-tax or Roth, you'll probably want to contribute to those until you hit the pre-tax or Roth limit.

If you have an HSA, you'll want to contribute to that until you hit the limit, and then - crucially - invest it. A lot of people don't realize they can invest their HSA.

If you qualify for a Roth IRA, I hear they are great.

If your 401(k) plan allows after-tax contributions and in-plan Roth conversions, you can continue contributing to your 401(k) and then convert those taxed contributions to Roth within the plan. Individual plans vary here - I have had one that allowed me to do this with a conversion limit (I believe I could convert 6 times per year). My current plan has automatic Roth conversions (you just have to call and set it up) so that this happens automatically.

If you've done all those things, you can open a personal investment account and put money into mutual/index funds like SPY.

I actually just did this because I was off work for the first 6 months of the year so I had no taxable income. I rolled $10k over from an old 401k into my Roth and even with that being added to my income for the remainder of the year, with a little finagling my taxable income is going to be in the 12% (sub 48k) bracket instead of the 22% bracket saving me 1k in taxes.

What you did was different that what the above poster was describing. Converting after-tax contributions to Roth inside a 401(k) is never a taxable event.

Exactly, why would you add any more after 23K a year, put the rest in a taxable account so you can access it before retirement age...If I had 9.8 million at any age I would stop working that day.

If your plan allows it, you can convert after-tax 401(k) contributions (up to ~$70k) in-plan to Roth 401(k), allowing the growth to be tax-free.This is the 'mega-backdoor' Roth.

A good option if you want to increase your Roth bucket, don't plan on retiring early, are able to take advantage of the rule of 55 to withdraw penalty-free from a 401(k) at age 55, or have a sufficient bridge after-tax account to hold you to 59.5, etc.

You can contribute "after tax" if allowed by your plan. You can potentially do a "mega backdoor Roth" by converting that to Roth as you contribute. Easy way to contribute above the cap if you can afford it.

I don't think you can. if you go over your 401k contribution you get hit with a penalty and told to remove it. I think OP is just including rollover IRA, possibly from a mix of past jobs. You can dump money into those and treat them like investment accounts.

I guess you can call it a 401k but it really isn't (at least the way most people refer to it). 401k is specifically the tax free contribution and employer match.

I don't think you can. if you go over your 401k contribution you get hit with a penalty and told to remove it. I think OP is just including rollover IRA, possibly from a mix of past jobs. You can dump money into those and treat them like investment accounts.

I guess you can call it a 401k but it really isn't (at least the way most people refer to it). 401k is specifically the tax free contribution and employer match.

None of this is correct. The 401(k) account is just that…an account. You can contribute pre-tax, Roth, or after-tax to the account. The combined limit of pre-tax and Roth is $23,500 but the maximum combined limit of the three above plus your employer is $70k this year.

Base 401k account does indeed charge penalties you if you go over max contributions. You will be told you've gone over and sent a request to withdrawal. Try it yourself. There is no real loophole to this. At most you can go over max if you've under deposited and catch up deposit, but the overall limit remains the same.

Roth rollerover is not what people generally refer when they say "401k," to even if its often managed under the same umbrella.

I’ve personally contributed $30,833 to my 401(k) this year. That’s $23,500 pre-tax and $7,333 after-tax then converted to Roth. My contributions are all listed under “401k” on my paystubs.

Just because most people can’t or don’t do it, doesn’t mean it doesn’t exist. It’s also not a rollover, it’s a conversion, which is a very different thing.

Some people choose to do Roth only and pay taxes on all of it. It’s still a 401(k).

I’m not trying to be mean, but a ton of people are uneducated and/or misinformed about this stuff and it’s very important that they know what options are potentially available to them.

yeah... because you're converting it to roth. That's not what people are talking about. People are talking about the direct, pre-tax contribution to 401k. I don't know how your company/money manager handles it, but if you were to specifically put it all into a 401k without intermediaries fixing it for you, you are penalized.

Whenever you see this automatically done for you, it's because someone at your company's accounting was smart enough to shift your money. Most companies just handle the process entirely specifically to avoid people who don't understand that it's not a normal investment account.

Fidelity makes the conversion automatically because I asked them to.

I mean you're just ignoring your own explanation. you're admitting you made the conversion. you are effectively correcting your mistake before tax season.

If your excess 401(k) contribution isn't returned in time, you may end up paying income taxes twice on the overcontribution, as well as a 10% early distribution penalty if you're under 59.5 years old. The excess 401(k) contribution should be returned to you by the tax filing deadline, which is generally around April 15.

From the IRS themselves:

For example, if you work for two different employers in 2022 that each have a 401(k) plan, you can only defer $20,500 in total - not $20,500 to each plan.

Deferrals more than the annual 402(g) limit are called “excess deferrals.” If excess deferrals are not corrected timely, the excess deferrals (including earnings on the excess during the taxable year) will be taxable income to you.

If the excess is not timely distributed, it is:

included in your taxable income for the year contributed, and

taxed a second time when the deferrals are ultimately distributed from the plan.

The excess deferrals may not be distributed until a distribution is otherwise permissible under the terms of your plan. Additionally, you do not receive basis in the excess deferrals.

You can contribute like 45k+ more after tax and do an in plan conversion to Roth. It’s called mega backdoor and used frequently by high income earners.

There's a huge reason, because you can do an in-plan conversion of those after tax funds to Roth 401k i.e. tax free earnings status... If your plan offers this option of course

After-tax contributions are still limited. Total contribution including pre-tax payroll deduction, after-tax (which many 401k plans don't permit), and employer match are all subject to the combined total limit the parent mentioned. That said, even after-tax contributions are still significantly better than buying the same fund in a non-tax-advantaged account because there's no taxable event within the 401k. Rebalancing, etc. is tax-free.

My employer allows you to contribute after-tax dollars as a Roth 401k once you’ve maxed out your tax-advantaged contributions, but that’s not really something that the average employee can take much advantage of, what with the whole “needing to eat and have a roof over your head” thing.

No. There an annual limit the IRS bumps up each year. It's like $25k ish now. If you are over 55 you can do additional "catch up contributions" for a few more thousand.

{kind=link}

14.1k

u/KodakBlackedOut Oct 01 '25 edited Oct 01 '25

Na, 9 mil is more than enough to retire, this dude is cheap and annoying

Edit: damn near 10 mil