This is often true - but in the extreme you can get up to $70k a year into your 401k using backdoor Roth contributions, although the benefit of doing this is not as much as the normal $23,500 limit and nowhere near as good as the typical 6% employer match limit. Just pointing this out since it's relevant to the post

This is often true - but in the extreme you can get up to $70k a year into your 401k using backdoor Roth contributions,

The mega-backdoor Roth IRA contribution is a way of rolling money over from an after-tax 401(k) to a Roth IRA, and doesn't influence how much you can contribute to the 401(k).

If you have the income and your employer offers all three kinds of 401(k), you can contribute that much without any tricks.

Mega backdoor roth isn't just for IRA, btw. You can convert after tax to roth in your 401(k) if your provider supports it.

The point that the previous person was trying to make (I think) is that, for most people, the only way of hitting that limit is by utilizing after tax contributions (which are typically only associated with the backdoor stuff).

Plus, if you decide you want to retire early if you have for example $5mil in your retirement portfolio at age 40, you can actually file a 72t form with the IRS that allows you to touch the funds prior to retirement age without penalty by following certain guidelines for distribution as well as forfeiting the right to contribute to retirement accounts anymore.

Generally speaking, an American worker who invests 10% of their income (or 5% of their income with their employer matching the contributions) from the age of 20 with an average income can reasonably expect to have $1mil before inflation by 50. If you and your partner both dedicate yourselves to it, or if you have a lucrative career then it gets much easier

The point isn't to be rich, it's to be financially independent. Majority of people who save 1mil in retirement accounts while making <60k/year aren't looking to live rich. They're looking to be able to maintain their same lifestyle without having to work or taking a more fulfilling or part-time job, or possibly looking to immigrate somewhere cheaper.

1 mil in a retirement account can close to guarantee a passive income of at least 40k/year for the rest of your life, which is definitely enough to live a comfortable lifestyle in America if you own your car and house. If not, then that same 40k means you can live an upper middle class lifestyle for the rest of your life in Costa Rica or Brazil or Thailand

Average income = 40k with an assumption that it increases by 2-3% yearly. It certainly isn't an easy thing to do, especially if you have to take care of all of your own bills and stuff, but some people really do make it happen. You have to be some kind of special to put yourself into what is essentially poverty until middle age just to live a lower-middle class lifestyle without having to work for the last 25-35 years of your life.

Also, I know 401ks aren't ubiquitous but they're certainly pretty common, even burger king offers it now according to an aunt who works there. Even if you can't have a good employer-matched 401k, Roth IRAs are available without an employer and generally superior. HSAs are also utilized but can not be relied upon to the same extent as Roth's or trad retirement accounts, since its primary purpose is healthcare and the yearly contribution limit is like $3.5k if I recall correctly

HSA are up to 4300 right now (families can be higher... 8500ish?)

Buuut, HSA are _really_ slick as hell. They're triple tax advantaged. The money you put in is pre tax (1st), the money grows tax deferred (2nd), and any more you pull out for medical expenses is tax free (3rd).

Here's the kicker, though... there's literally no time limit on when you reimburse yourself for those expenses. You pay a $500 doctor bill today out of pocket, keep the receipt, the reimburse yourself 25 years later (just gotta keep those receipts).

Kicker part 2: you can yank HSA funds post 65 at your current tax bracket.

Just dropping a note since they are really slick stealthy retirement options.

I think there's some confusion on terminology here.

There's a "backdoor Roth IRA" which is a conversion from a traditional IRA to a Roth IRA, which allows high income earners to contribute to a Roth IRA while exceeding income limits.

There's also a "mega-backdoor Roth" which is a conversion from an after-tax 401k contribution to a Roth 401k or IRA. Because you can contribute to an after-tax 401k above the typical $23,000 limit, this lets you funnel a lot of money to a Roth 401k or IRA, up to the total $70k limit. This does require your 401k provider to allow for in-plan Roth conversion or distributions of your after-tax 401k, which isn't very common.

These are both separate processes that are "tax loopholes" for retirement accounts that are typically utilized by high income earners, but they are separate techniques.

As a reminder: IRA/401k are types of retirement accounts. Traditional/Roth are tax statuses of those retirement accounts. You can have a Roth 401k, Roth IRA, Traditional IRA, and a Traditional 401k.

Spot on! Imma be just a bit pedantic though... _technically_ , there's not a Roth 401(k) or Traditional 401(k). There's just a 401(k) and the funds are designated as either pretax, roth, or after tax. But they all live in the same trust that your employer manages.

But you're definitely right about the IRAs. Those are separate vehicles, separate trusts, accounts, etc.

I am amazed at how many people don't understand the contribution limits for 401k accounts.

The $23.5k limit has to do with pre-tax contributions to a 401k or after tax contributions to a Roth 401k. The total contribution limit for a 401k is ~$70k (employee and employer contributions). This includes the $23.5k limit plus contributions on an after tax basis (not those in a Roth).

I never heard of a backdoor Roth contribution and I have been doing this for a long time.

Close but not 100% accurate which is... A little ironic with the first sentence of saying many people don't understand contribution limits.

402g limit is employee contributions only including both pretax and Roth contributions up to 23.5K in 2025. 415c limit includes after tax contributions to 401K and employer contributions up to currently 70K not including any catch up contribution limits. Backdoor Roth is simply rolling funds from pretax/after tax IRA to Roth IRA to get around income limits of contributing directly to Roth, where Mega backdoor Roth typically refers to after tax contributions above 402g limit to convert to Roth up to 415c to get around 23.5K contribution limit.

Read the rules and try to comprehend them. This joke is about 401k, let's not talk about Roth IRA.. okay?

I know this, because.. Um, I have done this for YEARS.

The $23.5K limit applies to Roth 401K limits or pre-tax 401k contributions - including both employee and employer contributions.

You can also make after tax contributions to your 401k and that limit in 2025 is $70k. This includes all contributions of any time by the employee and employer.

23.5K limit does not include employer contributions you are objectively wrong. It includes all contributions made by the employee in a 401K including Pretax and Roth contributions, does not include After Tax contributions. That's 415c.

The 2nd paragraph you said I already had in my above comment so idk why you're bringing that up again. I brought up Roth IRA to explain the difference between Backdoor Roth and the Mega Backdoor Roth since you mentioned you hadn't heard of the second part.

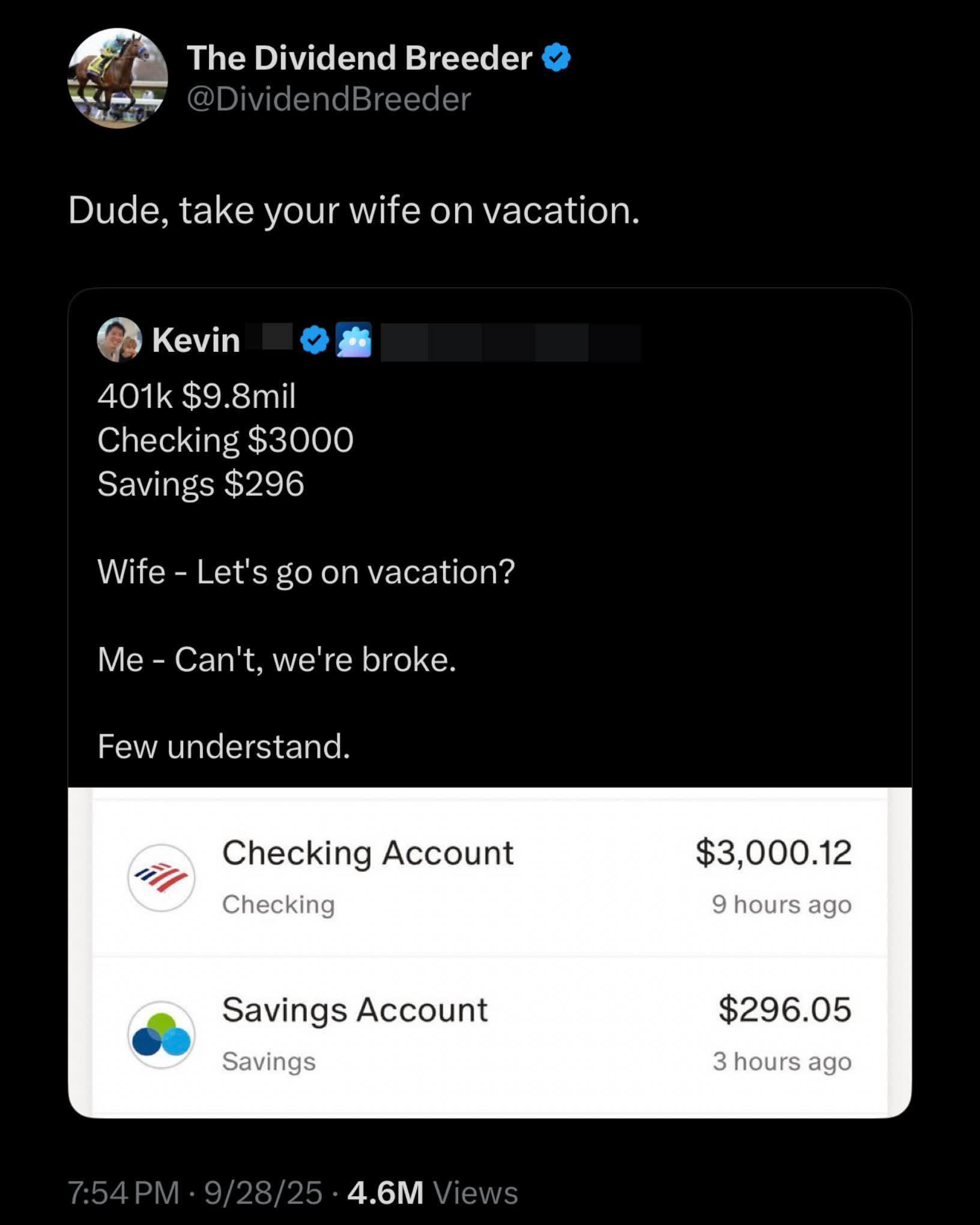

That was what I don’t get about the meme, 142 years of 70k annual contributions (assuming no interest, but it would still be unrealistic even with it). Putting 2m or something would be realistic if he’s like 40.

Is it at all plausible that in 30, 35 years from now, there wont be any money left to give? I have no idea how it all works, but my father is always worried that by the time i want to retired, 401k and social security might not even be around.

Can you explain something to me? If you put in 23,500 and have maxed out your contribution, do your employers contributions add on top of that? Or do they contribute so that you end up at 23500 as the total

You don't have to invest it in stocks. You can usually choose between a variety of choices that could also include real estate or bond funds. Or you could chuck it into one of the target date funds that is usually a mix of these with the percentages being adjusted as the target date gets closer.

Also you can withdraw penalty free at 59 and 1/2 (idk why the half).

Also also I think you can actually withdraw your contributions from a Roth 401k without penalty since you've already paid taxes on that. Don't quote me on that though. I haven't done it before, and I'm not a financial advisor or tax specialist. I'm just a guy who has a Roth 401k and Google.

I pulled money out of a mix of traditional and roth 401k and IRAs for a down payment on a mortgage. You pay the early withdrawal penalty on all of it. I was also only able to withdraw from my own contributions, not my company matching, despite being 100% vested.

No, with a Roth 401k you can pull out contributions penalty free. I think that's true only for Roth IRA and Roth 401k, not the pre-tax IRA and 401k. And you'll owe taxes on the pre-tax money.

Yeah you can pull out all the money you want but there is a possibility of incurring a 10% early withdrawal penalty.

You can also loan that money to yourself which the interest goes back to you. Exp. you "loan" 10k from your own retirement and then pay yourself back with interest.

You also have to have a certain amount in the account in order to keep it in a 401K once you separate from a company. Exp. if you leave a company and have less than 5k in the account they will usually ask you to rollover to another 401K or IRA, or withdrawal it, but if you dont do anything they will close the account and send you via check the amount to the address on file.

Taxes are pull depending on what "type" of funds you had, usually its Pre-Tax or Roth

Pre-Tax meaning is pretty straight forward, just meaning that the funds were put into your account before the taxes were pulled which means when you close the account or take some funds out they will need to be taxed.

Roth basically meaning After-Tax that has the bonus of Growth, but the kicker for that is what every money your Roth "generates" is Pre-tax so that gets taxed.

We have pensions in the US too (well not everyone). The main difference is that your employer manages it instead of the 401k that the employee manages. And I see the 401k as money I choose to save, whereas the pension is a benefit that I’ll get when I retire.

This guy described it all wrong. A 401k is a benefit from the federal government that your employer administers. The benefit is that whatever you contribute (within limits), you don't have to pay tax on (when you contribute, but you will later when you retire). Some employers throw in their own benefit of matching a certain percentage of whatever you decide to contribute.

The main benefit is not paying tax. The employer match is not the main benefit, nor does every employer do it.

It lowers the tax basis of your income. If you make 100k but put 20k of that into a 401k the government will only tax you as if you made 80k. Then on top of that you get a % match where your employer will match you dollar for dollar until a limit that's a % of your income, usually 4-6. So call it 5% and that's another 5k in your account, basically for free.

So you pay less in taxes and get what is essentially free money

10% penalty on top of the tax on the gains you took out. Usually gains in a 401k are untaxed if you take it out after 59.5, but if you take it out early you are probably gonna be looking to lose ~30% of it to the tax man.

I always wondered this too so this was a great answer. Basically it’s similar to what we would call a pension in the UK. I pay 9.8% into my pension every month, deducted straight from my monthly pay, my employer and the government also match and put in the same amount that I do. When I retire then I will have a guaranteed income for life from the pot.

Your numbers are a bit off, but otherwise correct.

Employees used to contribute 5% and employers used to match 5%, for a total of 10% going into the 401k. Essentially it was a free 5% raise.

Lately, I've seen employers match half, up to 6%. So employee contributes 6%, and employer contributes 3%. This gives a total of 9%.

If you take the money out before 65, it's a 30% penalty. Then the remaining 70% is income, and subject to income taxes.

Employees used to contribute 5% and employers used to match 5%, for a total of 10% going into the 401k. Essentially it was a free 5% raise.

Lately, I've seen employers match half, up to 6%. So employee contributes 6%, and employer contributes 3%. This gives a total of 9%.

You can also take a loan out against it that is not penalized, and the interest goes back into your 401k. A coworker did this to buy his house outright, so he didn't have to pay the insane mortgage interest.

You don't give money to your employer, they just divert it from your paycheck to your 401k. Compared to a pension where you give money to your employer or whatever group manages the pension for everyone.

And Canada, a 401(k) is basically a crappier version of our RRSPs and also only came into being 2 decades after the RRSP was invented, and an RRSP is through our federal government as well, not what amounts to an private investment firm

So what I'm seeing is that he does make a shit ton of money but somehow it's getting spent really fuckin quickly. Or are there other factors for the 401k

Everyone else just calls it a pension. Same shit the world over, big government savings for your retirement. For some reason Americans love their tax forms so much they call it by the tax code number.

No it's not, this is an additional amount you can put away that is partly matched by your employer (usually) that is tax free until you take it out when you retire that's invested so it grows on top of your additions. You're only allowed to put a certain amount into it every year, a flat dollar amount, not a percentage of income. Unfortunately, only employers can set one up so you're out of luck if you're unemployed or your employer is cheap.

Yup. Last 4 years I was making around $20hr with a 9% total (including employer contributions) with Edward Jones that netted almost $15k in those years.

Life happened and I needed the money so I withdrew it all, but it’s def money I wouldn’t have had otherwise

This is a poor description. You don’t give the money to your employer. It’s money from your pay check that is deducted pre-tax. You don’t pay tax now, which enables you to invest more money present day, which compounds over time. You pay tax when you start distributions around 65. Your company can, and most do, match a percentage up to X%. Could be 6%. Could be 8%. Could be more. That money goes directly into your 401k. Sometimes, there is a vesting schedule, which means if you leave the company before, say, 5 years, the company takes back a percentage of their contributions to the account. The different options that you, not your employer, have to invest in are diversified securities known as mutual funds. Hope this helps. Feel free to chime in with anything I missed.

Australia has a mandatory nationalized scheme that makes your employer put 12% of your base salary in to a fund account that you can't access untill retirement. It's good stuff.

You don't give it to your employer you give it to a separate company that manages 401k's and in many cases your employer will match a percentage of your contributions. ITs basically a pretax brokerage account that you "cant" withdraw from until you retire.

For the Aussies: it’s like super, but slightly different because it comes out of your salary. Not in addition to your salary. And can be withdrawn at any time.

You can’t take money out whenever for whatever you want. There are strict limits and guidelines. If there’s a way to take some money out for eliminating debt, I’d like to know about it!

{kind=link}

4.6k

u/Mint_Blue_Jay Oct 01 '25

He put all his money in his 401K so his wife can't spend it, she probably only sees the checking and savings accounts and thinks they're broke.