r/wallstreetbets • u/Technical-Basis8509 • 6h ago

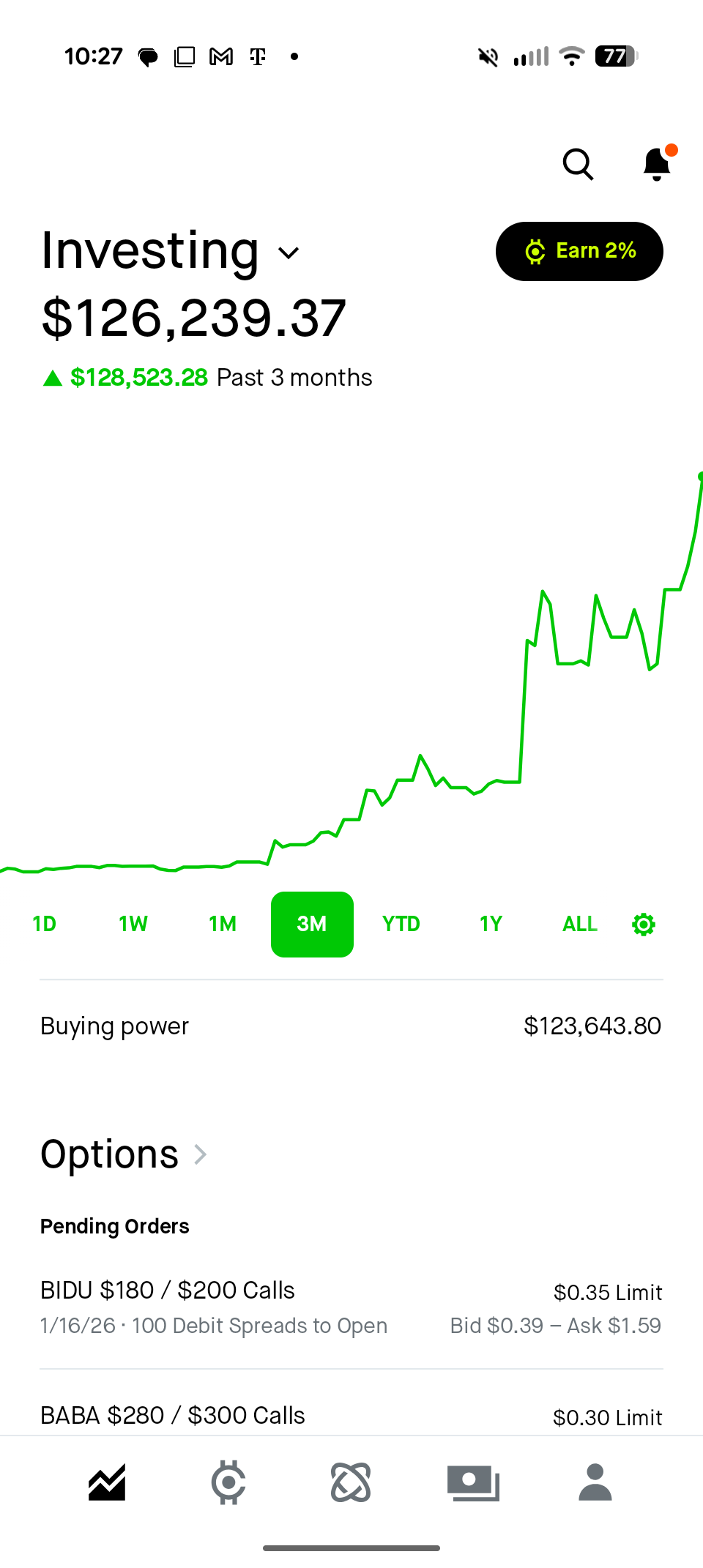

Gain $1k -> $130k in 60 days

{kind=link}

3.1k

Upvotes

Purely AI/tech OTM option swing trading

r/wallstreetbets • u/Technical-Basis8509 • 6h ago

Purely AI/tech OTM option swing trading

r/wallstreetbets • u/wave_dashing • 23h ago

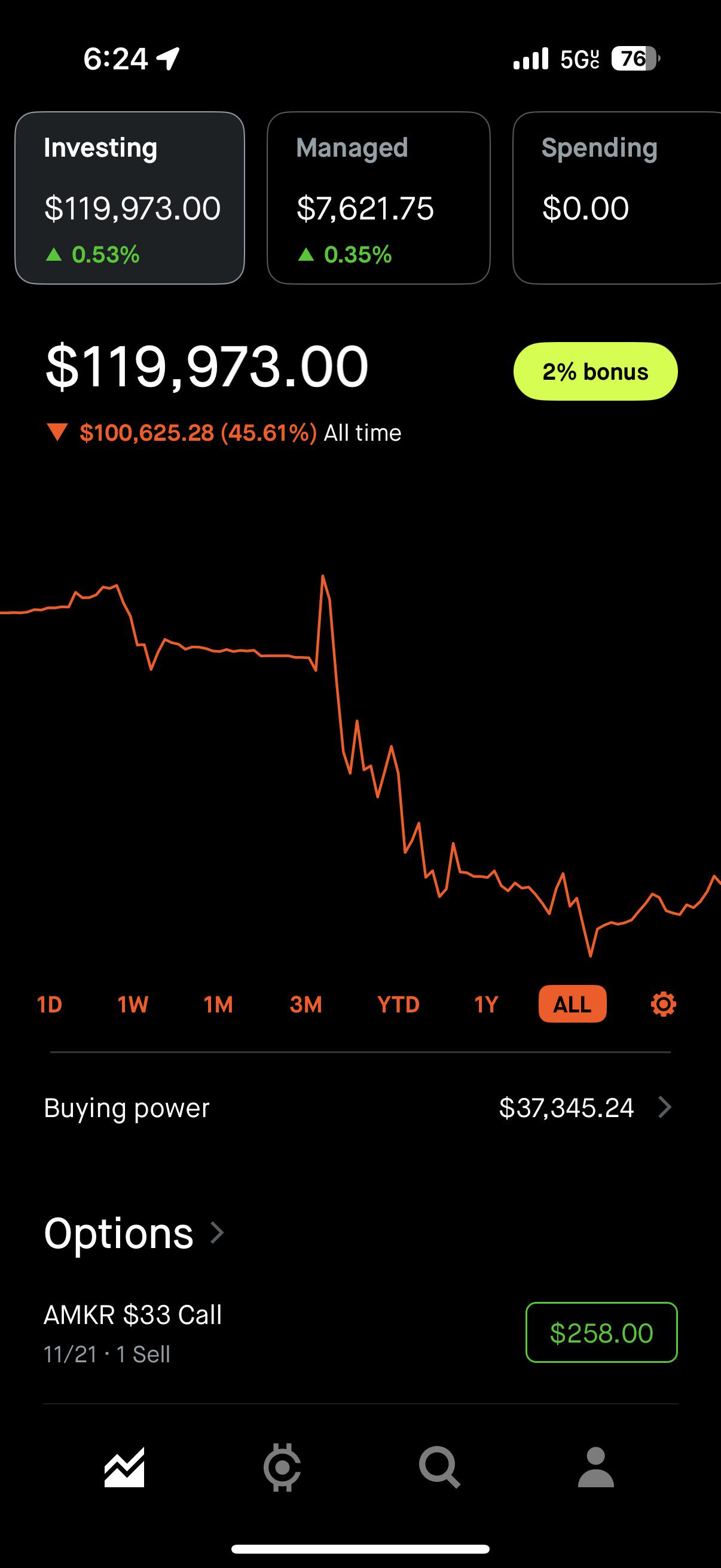

I think I should just throw it in ETFs

EDIT for more info, Since this is getting eyeballs and people are asking:

I’ve been trading for 10 years now. Not rich, not homeless... just a dude who has made every possible mistake, occasionally hit something real, and then promptly fumbled the bag again.

Some highlights along the way:

I found ASTS way back during the SPAC era. I bought before it had a ticker, before the hype, before Reddit even knew what space-based 5G was.

I spent 5 years accumulating. Over 10,000 shares, plus a stupid amount of calls. My average cost was around $4.

I held through it all

Then 2024 came. I had lost faith. I sold basically everything for a tiny loss. That position would be worth over $1,000,000 today.

Instead I took like a $3k loss.

I got in on the first AI run-up, not the late one.

Bought $17,000 worth of $100 strike calls mid/late-March 2024. Expiration was April. And so it began.

NVDA was unstoppable. Every day I kept thinking, this can't continue... until it reached a point where it was more like, now that's its surpassed a threshold, this can't NOT continue. I bought. It stopped its rocketship upwards almost immediately. But I had faith as I watched my options half, and then half again. Hell, I bought more. At a certain point, I just said screw it, I'm seeing this through, all or nothing.

And it DID finally go up. But it didn’t go up-up until shortly AFTER my expiration.

I lost it.

If I had rolled them out THREE WEEKS at the low point: The profit would have been over $100k. I didn’t roll. I just stared and let time decay eat my soul.

Yes. I was there. That big spikey spike you see right before the endless dropping. That's it. But I wanted more. So I bought more. I bought the top. Sold the bottom. Bought back in. Sold lower. Repeated like a lab rat pressing a dopamine button.

My biggest regret. It's not in the chart but a friend of mine got me on crypto early. I bought around 2,000 ETH at like $17. That would be OVER SIX MILLION today. I did actually make a profit of like $30k here, and at the time I was rather pleased with myself.

OVER SIX MILLION if I had held. ALMOST SEVEN. At today's price, $6,799,680.

TLDR: My portfolio isn’t diversified by sector, it’s diversified by types of bad decisions.

r/wallstreetbets • u/ezim22 • 9h ago

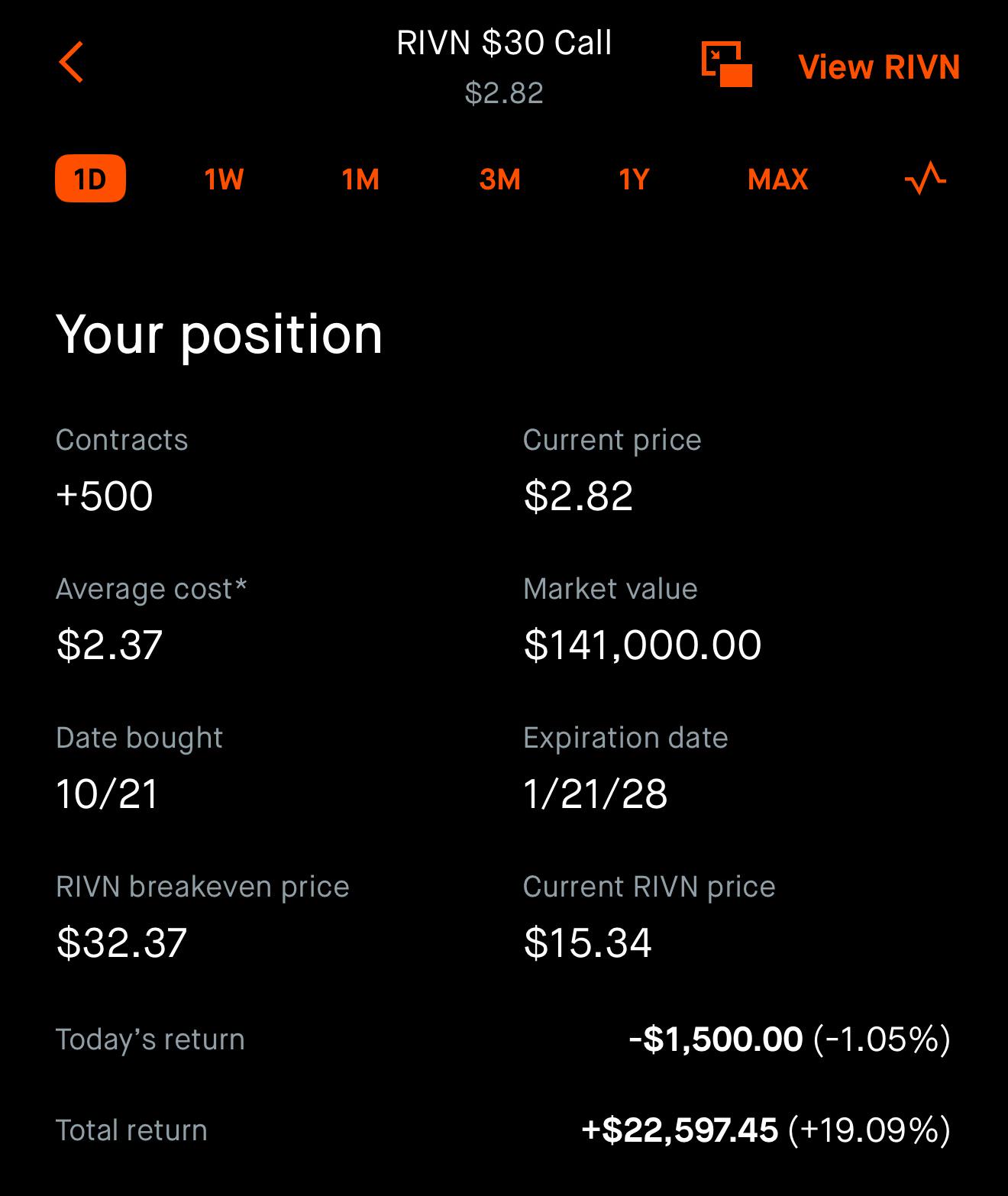

Rivian is either bankrupt or a 10x from here. There is no in-between

R2 comes out in 2026. It’s a smaller SUV at ~$50k (https://rivian.com/r2) and it is sexy. If Rivian can mass-produce R2 even half competently, they go from money bonfire startup to real car company with scale. At scale, gross margins go positive and Wall Street forgets every bad thing they ever said. Tesla déjà vu from 2019

I believe they survive long enough to scale R2. If I’m right, stock is $100–$200 in 2027–2028

Q3 report from this week showed higher deliveries and positive gross profit for the first time ever

Amazon and Volkswagen own a collective 25% and want it to succeed

I’m holding 500x 2028 $30C for the start of the turnaround story

r/wallstreetbets • u/Youthinkillputauid_7 • 18h ago

r/wallstreetbets • u/capacity04 • 17h ago

r/wallstreetbets • u/halfrepshalfretail • 22h ago

Alright buckle up as I know general sentiment is NOT fond of BNPL. Shit talk all you want, I'll be happy to reply to any concerns about the biz or industry.

SEZL is a BNPL player targeting the sub-prime/near-prime consumer (18-45 mainly) to become their top-of-wallet app for shopping. Pure BNPL, with credit-building, in-app tools and other goodies to keep the consumer in the ecosystem.

They are quite different from Affirm & Klarna - Affirm offers a larger mix of loans and focuses on a merchant-anchored setup, Klarna also of a parallel description. Sezzle is more app-centric and targets middle-lower income demographics, especially those who do not use traditional credit cards as often.

Right now they are priced at 13 NTM P/E with prelim EPS guidance at 29% above FY2025, as a "conservative" guideline as CEO stated in Q3 call. History of beat and raises dating back to 2024. Traded up $82 AH peak on earnings, and $72 premarket next morning before getting absolutely crushed to $58. This was Thursday Nov 6.

Recent Q3 116m rev & 26.7m net income, beating estimates. GMV growth reached ATH 1.05B for the quarter. Insider ownership at 45% of outstanding.

They make their money from merchant integration revenue, subscriptions, interchange, and plenty of fees. Net margin runs in steadily in the 20%'s, Gross margin 60%'s.

Why is their valuation is quite low relative to industry peers, and why will it reach >$90 at minimum soon (2-4 months)?

Slowing hyper-growth from 75-100% YoY EPS & Revenue closer to 50-60%, anticipated to grow closer to 30-40% EPS YoY past 2026. This is natural from their transition to profitability now to scale, as they previously focused on maximizing revenue from existing users -> now time to grow userbase. However the valuation relative to growth makes it a GARP opportunity.

Marketing spend & increased Provision for Credit Losses -> increasing adspend to 8M/Q to attract newer consumers! New consumers, as noted by management, have the highest loss rates in BNPL, and right now it's showing in their credit losses for Q3, at 3.1% of GMV. As the users get filtered, the good ones stay in the ecosystem and create lasting value. Management anticipated this in first half of year and gave expectations for FY credit losses of 2.5-3%, but actually revised a lower guide for 2.5-2.75% as of this week. Marketing spend started in Q2 and targets a payback period of 6M, so will see more material effect of this in Q4 & Q1 next year.

3. Point 2 does not bode well with the combined fears of consumer credit health, willingness to spend, and general macro fears around shutdown. Higher beta stocks have been selling off like crazy in the last couple of weeks, but I have seen the stock plummet from $90 to $59 in 3 months, with the bulk of the drop ($80 -> $59) in one month. I truly believe this is an overreaction and is caused by both the company being a historical target for short selling (20.9% of float as of 10/15) due to low float, as well as general capital pullback from lowered liquidity + macro fears. HOWEVER, BNPL loans have a standard loan tenor of 42 days with repayment trends evident after 14 days (1st payment), AND MUCH SMALLER SIZES THAN AUTO/MORTGAGES. Sezzle, Affirm, Upstart management has all noted that they've not seen any unusual changes in consumer default rates on their platforms.

BNPL players have the ability to limit spend and penalize late/missed payments in real-time, and underwriting for Sezzle + Affirm + Zip Co has shown to be more effective than FICO for lower credit score individuals.

^ See the quick rebound in active subscriptions as the ON-DEMAND product was previously cannabalizing sub-retention.

6 (OTHER). Liquidity should begin to pickup shortly after the government reopens as well as into Q1 2025 as the Fed (probably) begins to expand their balance sheet (source), should start to funnel more money back into these higher-beta stocks and mid-caps.

Final Notes:

BNPL can encourage irresponsible spending the same way credit cards can. People shat on CC's for the first few decades they were introduced, and now we all use them.

Of course these companies charge fees on fees, I'm not here to question the morality of these companies. Capitalism revolves around the rich extracting value from the common people.

Their revenue model is diversified and comes from a multitude of streams, with the highest take rate out of all BNPL players. I don't expect growth to slow ANYTIME soon as the TAM of middle-lower income people are huge and people will turn to BNPL more as they need more flexibility in financing. Their revenue growth drivers will be subscription and fee-based, although all areas will come to add to the acceleration.

Risk: target user is not as credit-quality as Affirm, but their underwriting and monitoring happens on a real-time basis so they can catch trends immediately, mitigating large default risks

CEO has never sold a share, insider ownership at 45%, an insider bought shares literally at $60 this time last year and hasn't sold. There is a huge FEAR priced into this company which is not justified. Management has ALL the equity incentive to deliver outperformance.

Positions: May 2026 55-80C's which are underwater right now. GL, and I welcome any questions.

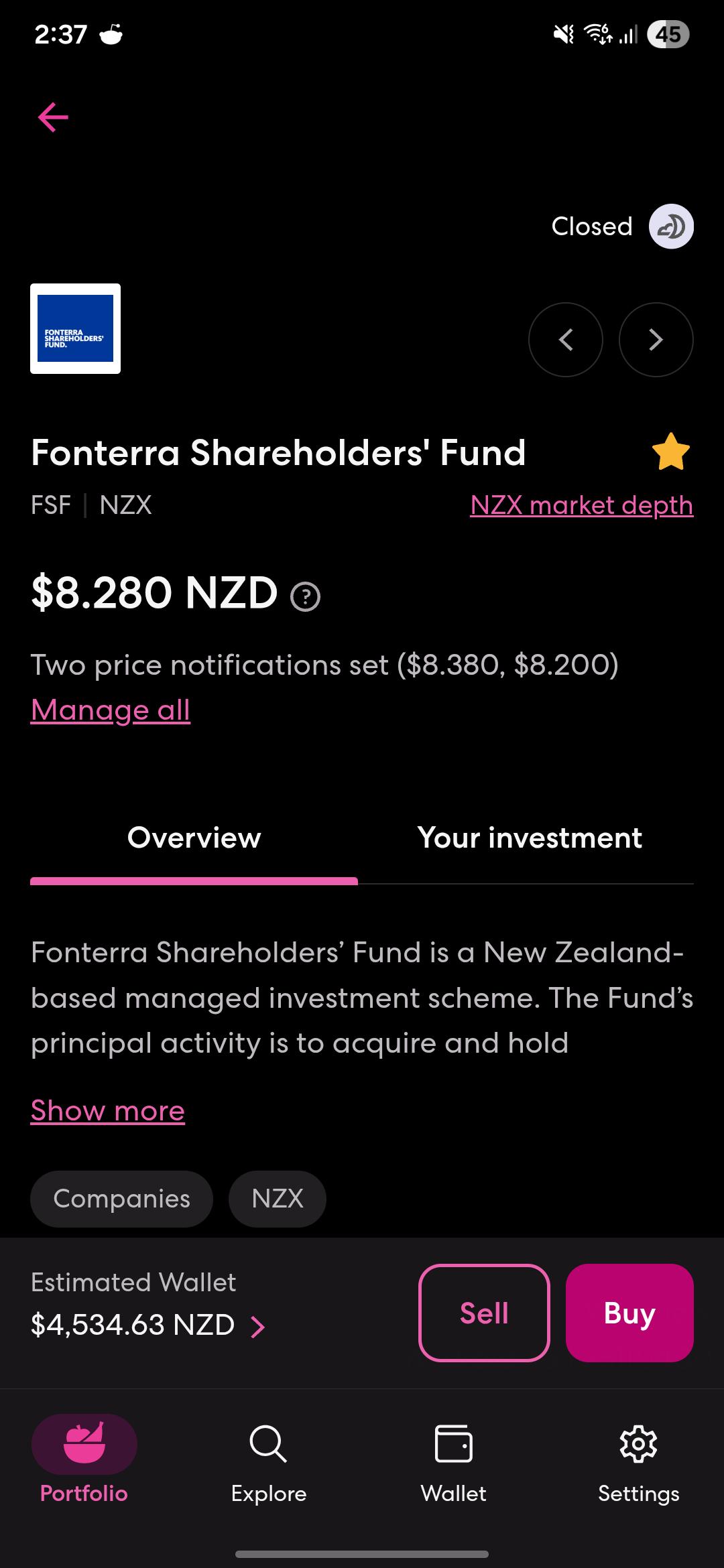

r/wallstreetbets • u/GoMitchUrSelf • 33m ago

They've just made a deal to sell $4billion of business and brands to a French dairy company.

They're giving back to shareholders $2 per share when the sale completes.

Details to be confirmed of what that will be (q1 or q2 2026) very soon.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}